One sign of a growing and healthy community is a thriving church. Whether you are reaping the harvest of planting a new church in your community or you’re a member of a well-established congregation, understanding how church loans work should be fundamental knowledge for church leadership. Unfortunately, guidance from reliable church financing information can be difficult to find when you need to stewardly plan a project.

Types of Church Loans

Short Term Mortgage

Long Term Mortgage

Unsecured Church Loan

Financing For

New Construction

Refinancing

Remodeling

Roadmap to Church Loans and Financials

As congregation numbers swell, church leadership is often forced to quickly remedy overcrowded worship spaces. This often means expansion or new construction, which can be very expensive. To complete a project, you will need to know the ins and outs of financing your new steel church building. We recently spoke with John Berardino, president of Griffin Capital Funding, about church loans and financing to provide some reliable guidelines for you to follow.

Before you rush to the bank for a new church loan, consider what potential lenders will be looking for before approving a loan. At the center of all loan agreements, of course, is trust. Lenders want to know they can trust a borrower to pay back the loan. So what’s the best way to show your church will be a consistent and reliable borrower? Berardino outlines a few of the basic requirements of the loan application process.

“We need to see your church has been in business for a minimum of three years,” Berardino said. He notes it’s possible to be approved with only a two-year history, but it requires an exception. “That’s our baseline requirement before you walk in the door.”

How Much Can Churches Borrow?

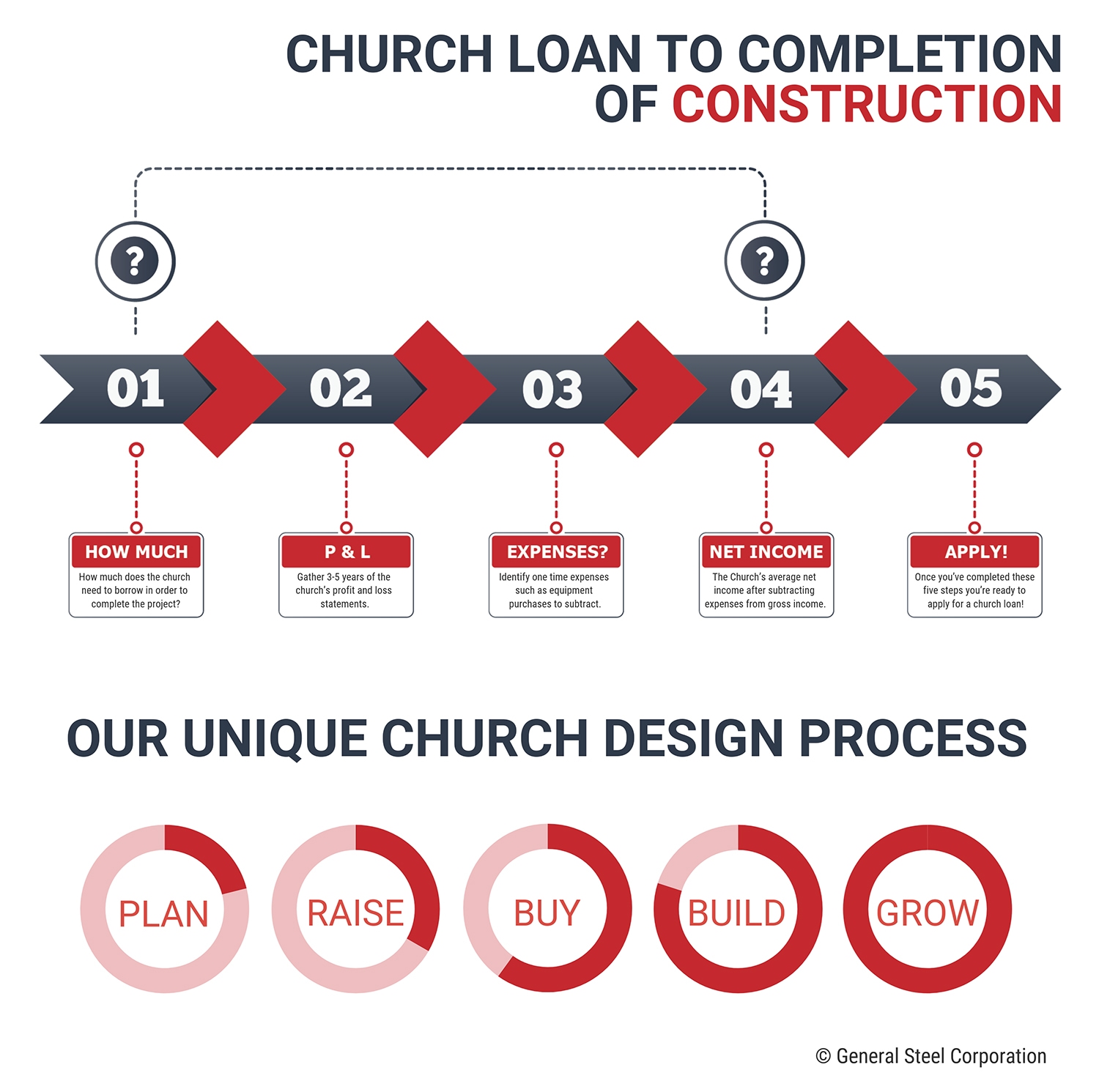

Submitting as much financial information as possible is preferable and can affect how much a church is able to borrow. A normal church can borrow up to about 4 times gross tithes and offerings, but it can be as high as six times its gross tithes and offerings.

Rule of Thumb

The maximum loan amount is based upon 4x-6x the church’s gross tithes and offerings (before expenses).

Berardino stresses, however, that, “any financial documentation can help the process, but other than the profit and loss statements, nothing else is required in the beginning for us to determine the ability of the church to service the debt.”

Make sure you identify the expense and the amount if the church has paid a lump sum for any expenditures over the past 3-5 years. These one-time expenses can be added back to the net income since they are not a typical expense such as staff salaries or utilities. In many cases, these one-time expenses can bring a church on the bubble of qualifying for a loan into satisfactory standing.

Example One Time Expenses

New Pews or Chairs

Repaving

Repairing Storm Damage

Do Not Qualify

Staff Salaries

Missions

Payroll Taxes

Is Lack of Credit an Issue?

Some churches are hesitant to apply because they lack a substantial credit history. According to Berardino, that’s not a problem. “Bottom line: the lack of church credit is never seen as a negative.” That’s encouraging for new and developing congregations that have yet to need extra funding.

Under normal circumstances, Griffin Capital does not pull the personal credit of the church leadership, so any credit problems they have personally are not usually taken into consideration.

Profit and Loss Statement

In addition to three years of business, Griffin Capital requires three years of profit and loss statements. Lenders need to see that funds are coming in that show the ability to make the payment. Operating budgets, attendance tracking and balance sheets can also make lenders more comfortable that your church is capable of handling the church loan.

Debt Income Ratio

Ultimately your church loan will come down to whether or not the lender is comfortable the church’s net income can reliably service the debt each month. Net income is how much money is left in church’s bank account after all expenses have been deducted. In simple terms, your new monthly payment multiplied by 12 months can only be a certain percentage of the church’s net income. Every lender is different, but a good target to aim at is 42% of annual net income.

Calculating Debt to Income Ratio

For example, if your church had an average net income of $100,000 over the past 3 years and your new loan payment is $3,500 per month, the church would satisfy the debt to income ratio of 42% ($3,500 x 12 months = $42,000 / $100,000 = 42%).

On the other hand, if the church only had an average net income of $90k over the past 3 years, identifying one-time expenses can be the difference between qualifying for the loan or not.

If you already own a parcel of land it can be used as collateral to help secure the loan. If you need to buy land as part of the project, this guide will help you navigate the process.

If you are in the planning phase of your project, our church design package is exactly what you need to visualize the project, begin a capital campaign and outline all project costs.

1. Mortgage: The first is a mortgage, which is common for large construction projects. Mortgage loans usually are more than $75,000 and require the borrower to put up current facilities or land as collateral.

Long Term vs. Short Term Mortgages

A long-term, fixed-rate mortgage locks in your monthly payments for a long period of time, providing a predictable but potentially costly payment schedule once interest is factored in.

A short-term, variable-rate mortgage has a sliding interest rate depending on national rates. This can lead to inconsistent payments but also allows the borrower to pay off the loan quickly if they’re capable.

2. Unsecured Church Loans: Another option is an unsecured church loan. These types of loans are most commonly used for smaller renovations or equipment upgrades. Since these loans are usually smaller than mortgages, they are more easily secured.

Popular Buildings for Churches

Browse hundreds of building kits from sanctuaries and gymnasiums to offices and schools.

Need help? We're listening. Let us guide you through your decision.

We have solutions no matter where your church is in the process of building. Click below to reach out to Griffin Capital about a church loan. You can also price one of our church buildings by giving us a call or online in 3 easy steps.